The Economic Transformation of the Black Sea Region. A Report by the Commission on the Black Sea (2)

By Panayotis GAVRAS. The Commission on the Black Sea

The Commission on the Black Sea presents a series of four policy-oriented reports which reassess the economic, social, regional political and military developments in the region.

This report is the first one, providing a better understanding of the parameters of the economic developments in the Black Sea. The Commission on the Black Sea does not take a collective position with this paper. This text represents only the views of its author.

Content

Executive Summary / (A) The Historical Context of Economic Development in the Black Sea Region / (B) The Economic Transformation of the Black Sea Region. Overview / (C) Implications of the Global Crisis for the Black Sea Region / (D) Challenges and Issues for the Black Sea Region / Long-Term Demographic Trends and Economic Reforms / Dealing with the Global Economic Crisis / The Evolution of Relations with External Players, and Especially Relations with the EU / Promoting Regional Cooperation / (E) Concluding Remarks / Policy Recommendations for the Economic Development of the Black Sea Region / (a) Recommendations for the Countries in the Black Sea Region / (b) Recommendations Designed to Promote Economic Developmentin the Black Sea Region Through Cooperation / (c) Recommendations for a European Union Approach to the Black Sea Region

(B) The Economic Transformation

of the Black Sea Region. Overview

Despite the adverse impact of the current crisis and the uncertainties it has generated, the Black Sea region is now a very different place than it was in 1999, or, for that matter, in 1989. This is certainly true from an economic perspective, and perhaps even more so in political and social terms3.

First, there has been a fundamental change in the economic structures within which people live and work in most of the Black Sea countries, and a shift from state-run to market-oriented economic systems.

This involved far-reaching economic liberalization and the creation of open markets. On the one hand the state sold off many assets and ceased to operate in many sectors of the economy and on the other hand the private sector grew rapidly to fill the vacuum left by the decline of the public sector.

It also branched out into entirely new areas, particularly in the services sector. Economic institutions were overhauled, prices and exchange rates were liberalized, and as a result there was both greater freedom and uncertainty.

While the extent of state involvement varies, all Black Sea countries now have market-oriented systems and focus to varying degrees on what are known as ‘second generation’ reforms which seek to preserve prospects for sustained growth (despite the current crisis ) and to strengthen state institutions, the market, and civil society4.

A second feature is the greater degree of prosperity throughout the region. Between 2002 and 2008 all the countries concerned posted positive growth.

Some of the smaller states maintained double-digit rates over much of the period and were also able to do a lot of ‘catching up’.

To be sure, the benefits of this economic growth have not been evenly distributed. Indeed, there is evidence that income distribution is more unequal, and that geographical disparities have increased.

Thus capital cities and major economic centres have reaped a greater share of the profits than rural or isolated areas.

However, the robust growth in the decade leading up to 2008 resulted in declining poverty rates in all of the countries in the region. In some cases this was rather impressive. Other key indicators such as health and education have also reflected the improvements in living standards.

Despite the fact that it is difficult to obtain up-to-date and accurate information, the trend clearly applies to all Black Sea countries and is supported by data that are easier to ascertain, including average wage levels and per capita income levels.

All the countries have witnessed large increases in average wages, particularly since 1999.

In the case of Greece and Turkey, the growth has been substantial, though wages were already at a relatively high level. However, in the case of former transition countries the changes have been dramatic, which is partly due to the low initial levels, with increases by a factor of 8–12 in nominal dollar terms. In real terms they have on average just about tripled.

After a period of relative stagnation in the non-transition states, and precipitous decline in the transition states during the 1990s, per capita incomes have risen dramatically. Between 1999 and 2008 they increased nearly five times in dollar terms, from about US$ 2,100 in 1999 to an estimated US$ 10,300 in 2008.

The third area in which the Black Sea region has seen significant changes is in that of the regional economic configurations.

In 1989 three countries were members of COMECON, Bulgaria, Romania, and the Soviet Union, to which six Black Sea countries belonged. The European Union (EU) was not contiguous with the Black Sea region, Greece was the sole regional state with EU membership, although Turkey had negotiated an EU Association Agreement. Both were also members of the OECD and other international organizations, though economic cooperation between them was at a low level.

In the case of the COMECON countries, the structure and extent of economic cooperation was imposed hegemonically.

There was no economic cooperation which included the entire Black Sea region. Today there is a surfeit of organizations seeking to promote regional cooperation and economic integration.

This plethora of initiatives testifies to the fact that there is a widespread understanding of the importance of regional cooperation, although so far it has manifested itself largely in formal terms.

Many initiatives include non-regional countries, and only a subset of Black Sea region states. Most of them are supported by external actors.

Even though they are not necessarily coercive, their value is questionable.

Only one organization covers the entire Black Sea region and has been established and developed locally, the Black Sea Economic Cooperation (BSEC). However, while in theory there is a greater degree of ‘ownership’ in comparison with externally generated cooperation schemes,

the extent to which BSEC has had an economic impact on the Black Sea region is also open to question.

If economic activity is defined in terms of the flow of goods, services, capital and people (and this does not only refer to labour),

the European Union is by far the most significant of the regional economic cooperation groups.

The reasons for this include its large membership, the degree of commitment that EU membership implies, the extent to which its member states have entrusted to the EU powers that are normally in the hands of sovereign governments, and the ensuing economic clout and political importance of the EU.

Although this is primarily a political issue, the relationship of a European country5 to the EU has significant economic ramifications.

It is influenced (i) by whether it is seeking membership or closer association with the EU, and (ii) by the extent to which the EU and its member states opt to engage and cooperate with it.

Today the EU extends to the shores of the Black Sea, where three countries are EU member states, and Turkey is an accession candidate6. In these countries economic policy is primarily determined by their EU rights and obligations.

Georgia, Moldova and Ukraine hope to obtain, but have not as yet received accession candidate status, and have been labelled ‘Neighbourhood’ countries along with Armenia and Azerbaijan, where the EU’s relations are determined by its European Neighbourhood Policy (ENP).

A key element of the ENP consists of deepening economic cooperation on the basis of EU rules and standards, and increasing trade and investment flows between the EU and the ENP countries.

Though much maligned, and perhaps deservedly so, ENP nevertheless represents the most far-reaching degree of engagement by the EU in the Black Sea region to date with countries without an EU membership perspective.

Thus in addition to growing economic relationships with EU members and accession candidates, the ENP countries are drawing closer to the EU, even though for the time being it seems unlikely that they will be able to join the EU.

Even for Russia, the country with the fewest institutional links, the EU has become a significant economic partner, since roughly half of Russian trade is with the EU.

Apart from the increased prosperity resulting from the 2000–2008 period of high growth, the economies of the region are now more open, interact with each other and are more in touch with the global economy in general, and western Europe in particular.

Flows of people, capital, goods and services have all increased, and the economic situation has been transformed in a significant and generally positive way. This is best seen in the business environment, which has grown in sophistication and now operates more smoothly.

In recent years a variety of systems has been devised to measure the state and the quality of the business environment7.

Since they are trying to quantify something which is essentially qualitative, they are largely subjective with scores based on perceptions, observations that are often of little value in statistical terms, and relative weightings. As such the individual scores should not be taken out of context, and it is better to look at them collectively prior to coming to certain conclusions.

In the countries of the Black Sea region, both individually and collectively, the indices pertaining to the business environment show that there has been an improvement over the last decade. In some cases the improvements have been moderate, and largely in absolute terms, whereas in other cases they have been rather dramatic, not only in absolute terms, but also when compared to other countries.

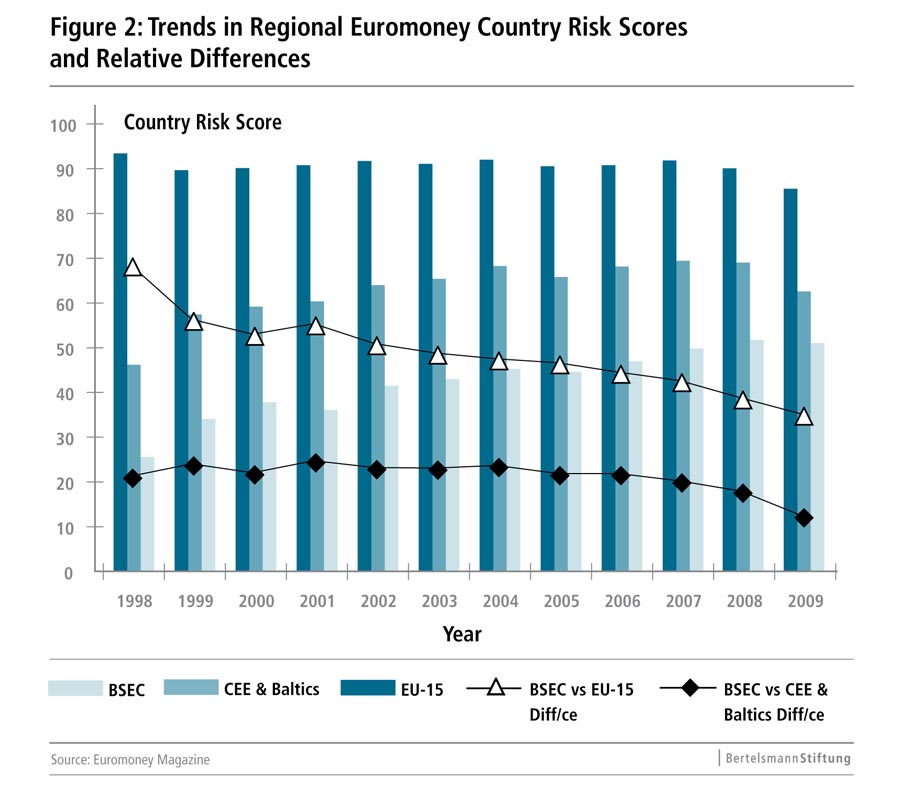

Figure 2 shows country risk scores based on Euromoney Magazine’s semi-annual Country Risk survey8.

Country risk9 is a particularly useful way of evaluating the business environment, since it quantifies the possible occurrence of a non-business event or a non-business situation which might threaten (i) the normal operation of a company (ii) the value of certain assets, and/or (iii) the profitability of loans and investments. A decline in country risk correlates directly with an improving business environment.

The figure shows an upward trend in the Black Sea region and convergence during the last decade.

In absolute terms, the region’s score improved steadily between 1998 and 2008, with a setback in 2009 due to the global crisis.

In relative terms, the difference between the Black Sea region and the original EU-15 on the one hand, and the Black Sea region and the Central European and Baltic countries that joined the EU in 2004 on the other hand, has continued to shrink in a consistent manner.

Although the Black Sea region continues to lag well behind EU-15 levels, the trend is a positive one and has persisted during the first part of the current global crisis.

Similarly, the trend based on the comparison with the CEE & Baltic countries has seen diminishing differences, even though most of the Black Sea countries were unable to reap the country risk benefits deriving from the EU accession process.

The improvement in the business environment is partly underscored by sovereign credit ratings11.

Whereas at the end of 1999 the Black Sea region had only one country with an investment grade rating, it now has four.

Significantly, every country in the Black Sea region has now ‘entered the market’ and received sovereign ratings. This is an indication of growing maturity and economic progress, since such ratings enable them to raise loans on the international capital markets and set benchmarks for the development of the domestic financial markets.

An even better and more easily measurable indicator of an attractive and favourable business and investment environment is foreign direct investment (FDI).

After languishing at around 1.0 % of GDP or even lower through most of the 1990s, between 2000 and 2008 FDI in the Black Sea region increased as a share of GDP from 1.1 % to 3.9 %. In dollar terms this is even more impressive, a sixteen-fold increase from U.S.$8 billion to an estimated U.S.$130 billion (see Figure 3).

3 These are arguably more significant, although this paper does not discuss them for reasons to do with focus, length, measurability, and the far greater expertise of other analysts.

4 On the transition process and the ‘first’ and ‘second’ generation reforms see 1) Tanzi,V. and Tsibouris, G. (2000): Fiscal reform over ten years of transition. IMF, Working Paper No. 00/113, and 2) Conference on Second Generation Reforms, Washington, D.C., 8–9 November 1999 at www.imf.org/external/pubs/ft/seminar/1999/reforms/index.htm. I 9

5 Despite the EU’s ambivalence and the many and varied opinions on the matter, in this paper all the countries included in the Commission on the Black Sea are assumed to be part of Europe.

6 BSEC members Albania and Serbia, which are not included in this survey, are currently potential EU accession candidates.

7 An increasing array of publications lists and ranks the various countries. The most reliable ones include (i) the World Bank’s Doing Business Reports, which measure the ease of doing business, (ii) Transparency International’s Corruption Perceptions Index Reports, which measure the quality of transparency and the extent of corruption, and (iii) EBRD’s Transition Reports, which focus on the business environment and the extent to which countries are seen to function as ‘market economies’.

8 Euromoney’s Country Risk survey is arguably the most comprehensive index and covers nine categories. Figure 2 provides simplified regional representations based only on arithmetic averages. They are not weighted to take into account the relative size of an economy or other factors. The figure was prepared solely for illustrative purposes, and shows the evolution of country risk scores over time. The bars show that an increased score signifies an improvement (i.e. decrease) in country risk. 100 represents the maximum (i.e lowest) risk score. Declining lines indicate decreasing differences in country risk scores between the regions under comparison (i.e. the convergence of scores and country risk levels).

9 In the present context country risk is defined as the weighted sum of a collection of scores including (i) macroeconomic performance and stability, (ii) security, political and social stability, (iii) perceptions of public and private governance, including implementation capacity, transparency, and corruption, (iv) the quality and clarity of a country’s legal and tax framework, and the quality of its implementation, (v) and the general ability of economic entities to operate in a smooth manner.

10 Czech Republic, Estonia, Hungary, Latvia, Lithuania, Poland, Slovakia, Slovenia. They are labelled ‘CEE & Baltics’ in the chart. These countries are frequently used for comparison with the Black Sea region since they are also former transition countries. However, they were more advanced in economical terms and are thought to have completed the ‘transition’ faster.

11 Long-term sovereign credit ratings, which define creditworthiness, are a useful measurement of the business environment despite (i) the justifiable criticism which has been levelled at them during the current global crisis, and (ii) their biased way of assessing emerging markets. They are easy to recognize and compare, and measure aspects of country risk. Investment grade refers to a sovereign credit rating of Baa3 or higher issued by Moody’s, and BBB- or higher issued by Standard & Poor’s or Fitch.

About the author

Panayotis Gavras has been with the Black Sea Trade and Development Bank (BSTDB) since its start-up in 1999. He is currently co-Head of the Policy and Strategy Department and has directed a variety of strategic and operational activities, including the preparation of country strategies, economic analysis of member countries.

He has also directed the Bank’s economic research on the Black Sea Region. Prior to the BSTDB, he worked at the World Bank and the National Foundation for the Reception and Resettlement of Repatriated Greeks. He holds a Bachelor of Arts degree from Princeton University, and a Masters in Public Policy from the Kennedy School of Government.

sup

More on the topic

- 30.05.2013 The South Caucasus countries and their security dimension

- 23.02.2011 Implications of the Global Crisis for the Black Sea Region. A Report by the Commission on the Black Sea (3)

- 31.01.2011 European Parliament resolution on an EU Strategy for the Black Sea (2)

- 27.01.2011 European Parliament resolution on an EU Strategy for the Black Sea (1)

- 10.01.2011 The Current State of Economic Development in the Black Sea Region. A Report by the Commission on the Black Sea (1)